- What is Elasticsearch?

- What’s new in 8.10

- Set up Elasticsearch

- Installing Elasticsearch

- Run Elasticsearch locally

- Configuring Elasticsearch

- Important Elasticsearch configuration

- Secure settings

- Auditing settings

- Circuit breaker settings

- Cluster-level shard allocation and routing settings

- Miscellaneous cluster settings

- Cross-cluster replication settings

- Discovery and cluster formation settings

- Field data cache settings

- Health Diagnostic settings

- Index lifecycle management settings

- Data stream lifecycle settings

- Index management settings

- Index recovery settings

- Indexing buffer settings

- License settings

- Local gateway settings

- Logging

- Machine learning settings

- Monitoring settings

- Node

- Networking

- Node query cache settings

- Search settings

- Security settings

- Shard request cache settings

- Snapshot and restore settings

- Transforms settings

- Thread pools

- Watcher settings

- Advanced configuration

- Important system configuration

- Bootstrap Checks

- Heap size check

- File descriptor check

- Memory lock check

- Maximum number of threads check

- Max file size check

- Maximum size virtual memory check

- Maximum map count check

- Client JVM check

- Use serial collector check

- System call filter check

- OnError and OnOutOfMemoryError checks

- Early-access check

- G1GC check

- All permission check

- Discovery configuration check

- Bootstrap Checks for X-Pack

- Starting Elasticsearch

- Stopping Elasticsearch

- Discovery and cluster formation

- Add and remove nodes in your cluster

- Full-cluster restart and rolling restart

- Remote clusters

- Plugins

- Upgrade Elasticsearch

- Index modules

- Mapping

- Text analysis

- Overview

- Concepts

- Configure text analysis

- Built-in analyzer reference

- Tokenizer reference

- Token filter reference

- Apostrophe

- ASCII folding

- CJK bigram

- CJK width

- Classic

- Common grams

- Conditional

- Decimal digit

- Delimited payload

- Dictionary decompounder

- Edge n-gram

- Elision

- Fingerprint

- Flatten graph

- Hunspell

- Hyphenation decompounder

- Keep types

- Keep words

- Keyword marker

- Keyword repeat

- KStem

- Length

- Limit token count

- Lowercase

- MinHash

- Multiplexer

- N-gram

- Normalization

- Pattern capture

- Pattern replace

- Phonetic

- Porter stem

- Predicate script

- Remove duplicates

- Reverse

- Shingle

- Snowball

- Stemmer

- Stemmer override

- Stop

- Synonym

- Synonym graph

- Trim

- Truncate

- Unique

- Uppercase

- Word delimiter

- Word delimiter graph

- Character filters reference

- Normalizers

- Index templates

- Data streams

- Ingest pipelines

- Example: Parse logs

- Enrich your data

- Processor reference

- Append

- Attachment

- Bytes

- Circle

- Community ID

- Convert

- CSV

- Date

- Date index name

- Dissect

- Dot expander

- Drop

- Enrich

- Fail

- Fingerprint

- Foreach

- Geo-grid

- GeoIP

- Grok

- Gsub

- HTML strip

- Inference

- Join

- JSON

- KV

- Lowercase

- Network direction

- Pipeline

- Redact

- Registered domain

- Remove

- Rename

- Reroute

- Script

- Set

- Set security user

- Sort

- Split

- Trim

- Uppercase

- URL decode

- URI parts

- User agent

- Aliases

- Search your data

- Collapse search results

- Filter search results

- Highlighting

- Long-running searches

- Near real-time search

- Paginate search results

- Retrieve inner hits

- Retrieve selected fields

- Search across clusters

- Search multiple data streams and indices

- Search shard routing

- Search templates

- Search with synonyms

- Sort search results

- kNN search

- Semantic search

- Searching with query rules

- Query DSL

- Aggregations

- Bucket aggregations

- Adjacency matrix

- Auto-interval date histogram

- Categorize text

- Children

- Composite

- Date histogram

- Date range

- Diversified sampler

- Filter

- Filters

- Frequent item sets

- Geo-distance

- Geohash grid

- Geohex grid

- Geotile grid

- Global

- Histogram

- IP prefix

- IP range

- Missing

- Multi Terms

- Nested

- Parent

- Random sampler

- Range

- Rare terms

- Reverse nested

- Sampler

- Significant terms

- Significant text

- Terms

- Time series

- Variable width histogram

- Subtleties of bucketing range fields

- Metrics aggregations

- Pipeline aggregations

- Average bucket

- Bucket script

- Bucket count K-S test

- Bucket correlation

- Bucket selector

- Bucket sort

- Change point

- Cumulative cardinality

- Cumulative sum

- Derivative

- Extended stats bucket

- Inference bucket

- Max bucket

- Min bucket

- Moving function

- Moving percentiles

- Normalize

- Percentiles bucket

- Serial differencing

- Stats bucket

- Sum bucket

- Bucket aggregations

- Geospatial analysis

- EQL

- ES|QL

- Syntax reference

- Source commands

- Processing commands

- Functions

ABSACOSASINATANATAN2AUTO_BUCKETCASECEILCIDR_MATCHCOALESCECONCATCOSCOSHDATE_EXTRACTDATE_FORMATDATE_PARSEDATE_TRUNCEFLOORGREATESTIS_FINITEIS_INFINITEIS_NANLEASTLEFTLENGTHLOG10LTRIMMV_AVGMV_CONCATMV_COUNTMV_DEDUPEMV_MAXMV_MEDIANMV_MINMV_SUMNOWPIPOWRIGHTROUNDRTRIMSINSINHSPLITSQRTSTARTS_WITHSUBSTRINGTANTANHTAUTO_BOOLEANTO_DATETIMETO_DEGREESTO_DOUBLETO_INTEGERTO_IPTO_LONGTO_RADIANSTO_STRINGTO_UNSIGNED_LONGTO_VERSIONTRIM

- Aggregation functions

- Multivalued fields

- Metadata fields

- Task management

- SQL

- Overview

- Getting Started with SQL

- Conventions and Terminology

- Security

- SQL REST API

- SQL Translate API

- SQL CLI

- SQL JDBC

- SQL ODBC

- SQL Client Applications

- SQL Language

- Functions and Operators

- Comparison Operators

- Logical Operators

- Math Operators

- Cast Operators

- LIKE and RLIKE Operators

- Aggregate Functions

- Grouping Functions

- Date/Time and Interval Functions and Operators

- Full-Text Search Functions

- Mathematical Functions

- String Functions

- Type Conversion Functions

- Geo Functions

- Conditional Functions And Expressions

- System Functions

- Reserved keywords

- SQL Limitations

- Scripting

- Data management

- ILM: Manage the index lifecycle

- Tutorial: Customize built-in policies

- Tutorial: Automate rollover

- Index management in Kibana

- Overview

- Concepts

- Index lifecycle actions

- Configure a lifecycle policy

- Migrate index allocation filters to node roles

- Troubleshooting index lifecycle management errors

- Start and stop index lifecycle management

- Manage existing indices

- Skip rollover

- Restore a managed data stream or index

- Data tiers

- Autoscaling

- Monitor a cluster

- Roll up or transform your data

- Set up a cluster for high availability

- Snapshot and restore

- Secure the Elastic Stack

- Elasticsearch security principles

- Start the Elastic Stack with security enabled automatically

- Manually configure security

- Updating node security certificates

- User authentication

- Built-in users

- Service accounts

- Internal users

- Token-based authentication services

- User profiles

- Realms

- Realm chains

- Security domains

- Active Directory user authentication

- File-based user authentication

- LDAP user authentication

- Native user authentication

- OpenID Connect authentication

- PKI user authentication

- SAML authentication

- Kerberos authentication

- JWT authentication

- Integrating with other authentication systems

- Enabling anonymous access

- Looking up users without authentication

- Controlling the user cache

- Configuring SAML single-sign-on on the Elastic Stack

- Configuring single sign-on to the Elastic Stack using OpenID Connect

- User authorization

- Built-in roles

- Defining roles

- Role restriction

- Security privileges

- Document level security

- Field level security

- Granting privileges for data streams and aliases

- Mapping users and groups to roles

- Setting up field and document level security

- Submitting requests on behalf of other users

- Configuring authorization delegation

- Customizing roles and authorization

- Enable audit logging

- Restricting connections with IP filtering

- Securing clients and integrations

- Operator privileges

- Troubleshooting

- Some settings are not returned via the nodes settings API

- Authorization exceptions

- Users command fails due to extra arguments

- Users are frequently locked out of Active Directory

- Certificate verification fails for curl on Mac

- SSLHandshakeException causes connections to fail

- Common SSL/TLS exceptions

- Common Kerberos exceptions

- Common SAML issues

- Internal Server Error in Kibana

- Setup-passwords command fails due to connection failure

- Failures due to relocation of the configuration files

- Limitations

- Watcher

- Command line tools

- elasticsearch-certgen

- elasticsearch-certutil

- elasticsearch-create-enrollment-token

- elasticsearch-croneval

- elasticsearch-keystore

- elasticsearch-node

- elasticsearch-reconfigure-node

- elasticsearch-reset-password

- elasticsearch-saml-metadata

- elasticsearch-service-tokens

- elasticsearch-setup-passwords

- elasticsearch-shard

- elasticsearch-syskeygen

- elasticsearch-users

- How to

- Troubleshooting

- Fix common cluster issues

- Diagnose unassigned shards

- Add a missing tier to the system

- Allow Elasticsearch to allocate the data in the system

- Allow Elasticsearch to allocate the index

- Indices mix index allocation filters with data tiers node roles to move through data tiers

- Not enough nodes to allocate all shard replicas

- Total number of shards for an index on a single node exceeded

- Total number of shards per node has been reached

- Troubleshooting corruption

- Fix data nodes out of disk

- Fix master nodes out of disk

- Fix other role nodes out of disk

- Start index lifecycle management

- Start Snapshot Lifecycle Management

- Restore from snapshot

- Multiple deployments writing to the same snapshot repository

- Addressing repeated snapshot policy failures

- Troubleshooting an unstable cluster

- Troubleshooting discovery

- Troubleshooting monitoring

- Troubleshooting transforms

- Troubleshooting Watcher

- Troubleshooting searches

- Troubleshooting shards capacity health issues

- REST APIs

- API conventions

- Common options

- REST API compatibility

- Autoscaling APIs

- Behavioral Analytics APIs

- Compact and aligned text (CAT) APIs

- cat aliases

- cat allocation

- cat anomaly detectors

- cat component templates

- cat count

- cat data frame analytics

- cat datafeeds

- cat fielddata

- cat health

- cat indices

- cat master

- cat nodeattrs

- cat nodes

- cat pending tasks

- cat plugins

- cat recovery

- cat repositories

- cat segments

- cat shards

- cat snapshots

- cat task management

- cat templates

- cat thread pool

- cat trained model

- cat transforms

- Cluster APIs

- Cluster allocation explain

- Cluster get settings

- Cluster health

- Health

- Cluster reroute

- Cluster state

- Cluster stats

- Cluster update settings

- Nodes feature usage

- Nodes hot threads

- Nodes info

- Prevalidate node removal

- Nodes reload secure settings

- Nodes stats

- Cluster Info

- Pending cluster tasks

- Remote cluster info

- Task management

- Voting configuration exclusions

- Create or update desired nodes

- Get desired nodes

- Delete desired nodes

- Get desired balance

- Reset desired balance

- Cross-cluster replication APIs

- Data stream APIs

- Document APIs

- Enrich APIs

- EQL APIs

- Features APIs

- Fleet APIs

- Find structure API

- Graph explore API

- Index APIs

- Alias exists

- Aliases

- Analyze

- Analyze index disk usage

- Clear cache

- Clone index

- Close index

- Create index

- Create or update alias

- Create or update component template

- Create or update index template

- Create or update index template (legacy)

- Delete component template

- Delete dangling index

- Delete alias

- Delete index

- Delete index template

- Delete index template (legacy)

- Exists

- Field usage stats

- Flush

- Force merge

- Get alias

- Get component template

- Get field mapping

- Get index

- Get index settings

- Get index template

- Get index template (legacy)

- Get mapping

- Import dangling index

- Index recovery

- Index segments

- Index shard stores

- Index stats

- Index template exists (legacy)

- List dangling indices

- Open index

- Refresh

- Resolve index

- Rollover

- Shrink index

- Simulate index

- Simulate template

- Split index

- Unfreeze index

- Update index settings

- Update mapping

- Index lifecycle management APIs

- Create or update lifecycle policy

- Get policy

- Delete policy

- Move to step

- Remove policy

- Retry policy

- Get index lifecycle management status

- Explain lifecycle

- Start index lifecycle management

- Stop index lifecycle management

- Migrate indices, ILM policies, and legacy, composable and component templates to data tiers routing

- Ingest APIs

- Info API

- Licensing APIs

- Logstash APIs

- Machine learning APIs

- Machine learning anomaly detection APIs

- Add events to calendar

- Add jobs to calendar

- Close jobs

- Create jobs

- Create calendars

- Create datafeeds

- Create filters

- Delete calendars

- Delete datafeeds

- Delete events from calendar

- Delete filters

- Delete forecasts

- Delete jobs

- Delete jobs from calendar

- Delete model snapshots

- Delete expired data

- Estimate model memory

- Flush jobs

- Forecast jobs

- Get buckets

- Get calendars

- Get categories

- Get datafeeds

- Get datafeed statistics

- Get influencers

- Get jobs

- Get job statistics

- Get model snapshots

- Get model snapshot upgrade statistics

- Get overall buckets

- Get scheduled events

- Get filters

- Get records

- Open jobs

- Post data to jobs

- Preview datafeeds

- Reset jobs

- Revert model snapshots

- Start datafeeds

- Stop datafeeds

- Update datafeeds

- Update filters

- Update jobs

- Update model snapshots

- Upgrade model snapshots

- Machine learning data frame analytics APIs

- Create data frame analytics jobs

- Delete data frame analytics jobs

- Evaluate data frame analytics

- Explain data frame analytics

- Get data frame analytics jobs

- Get data frame analytics jobs stats

- Preview data frame analytics

- Start data frame analytics jobs

- Stop data frame analytics jobs

- Update data frame analytics jobs

- Machine learning trained model APIs

- Clear trained model deployment cache

- Create or update trained model aliases

- Create part of a trained model

- Create trained models

- Create trained model vocabulary

- Delete trained model aliases

- Delete trained models

- Get trained models

- Get trained models stats

- Infer trained model

- Start trained model deployment

- Stop trained model deployment

- Update trained model deployment

- Migration APIs

- Node lifecycle APIs

- Query rules APIs

- Reload search analyzers API

- Repositories metering APIs

- Rollup APIs

- Script APIs

- Search APIs

- Search Application APIs

- Searchable snapshots APIs

- Security APIs

- Authenticate

- Change passwords

- Clear cache

- Clear roles cache

- Clear privileges cache

- Clear API key cache

- Clear service account token caches

- Create API keys

- Create or update application privileges

- Create or update role mappings

- Create or update roles

- Create or update users

- Create service account tokens

- Delegate PKI authentication

- Delete application privileges

- Delete role mappings

- Delete roles

- Delete service account token

- Delete users

- Disable users

- Enable users

- Enroll Kibana

- Enroll node

- Get API key information

- Get application privileges

- Get builtin privileges

- Get role mappings

- Get roles

- Get service accounts

- Get service account credentials

- Get token

- Get user privileges

- Get users

- Grant API keys

- Has privileges

- Invalidate API key

- Invalidate token

- OpenID Connect prepare authentication

- OpenID Connect authenticate

- OpenID Connect logout

- Query API key information

- Update API key

- Bulk update API keys

- SAML prepare authentication

- SAML authenticate

- SAML logout

- SAML invalidate

- SAML complete logout

- SAML service provider metadata

- SSL certificate

- Activate user profile

- Disable user profile

- Enable user profile

- Get user profiles

- Suggest user profile

- Update user profile data

- Has privileges user profile

- Create Cross-Cluster API key

- Update Cross-Cluster API key

- Snapshot and restore APIs

- Snapshot lifecycle management APIs

- SQL APIs

- Synonyms APIs

- Transform APIs

- Usage API

- Watcher APIs

- Definitions

- Migration guide

- Release notes

- Elasticsearch version 8.11.0

- Elasticsearch version 8.10.0

- Elasticsearch version 8.9.2

- Elasticsearch version 8.9.1

- Elasticsearch version 8.9.0

- Elasticsearch version 8.8.2

- Elasticsearch version 8.8.1

- Elasticsearch version 8.8.0

- Elasticsearch version 8.7.1

- Elasticsearch version 8.7.0

- Elasticsearch version 8.6.2

- Elasticsearch version 8.6.1

- Elasticsearch version 8.6.0

- Elasticsearch version 8.5.3

- Elasticsearch version 8.5.2

- Elasticsearch version 8.5.1

- Elasticsearch version 8.5.0

- Elasticsearch version 8.4.3

- Elasticsearch version 8.4.2

- Elasticsearch version 8.4.1

- Elasticsearch version 8.4.0

- Elasticsearch version 8.3.3

- Elasticsearch version 8.3.2

- Elasticsearch version 8.3.1

- Elasticsearch version 8.3.0

- Elasticsearch version 8.2.3

- Elasticsearch version 8.2.2

- Elasticsearch version 8.2.1

- Elasticsearch version 8.2.0

- Elasticsearch version 8.1.3

- Elasticsearch version 8.1.2

- Elasticsearch version 8.1.1

- Elasticsearch version 8.1.0

- Elasticsearch version 8.0.1

- Elasticsearch version 8.0.0

- Elasticsearch version 8.0.0-rc2

- Elasticsearch version 8.0.0-rc1

- Elasticsearch version 8.0.0-beta1

- Elasticsearch version 8.0.0-alpha2

- Elasticsearch version 8.0.0-alpha1

- Dependencies and versions

Serial differencing aggregationedit

Serial differencing is a technique where values in a time series are subtracted from itself at different time lags or periods. For example, the datapoint f(x) = f(xt) - f(xt-n), where n is the period being used.

A period of 1 is equivalent to a derivative with no time normalization: it is simply the change from one point to the next. Single periods are useful for removing constant, linear trends.

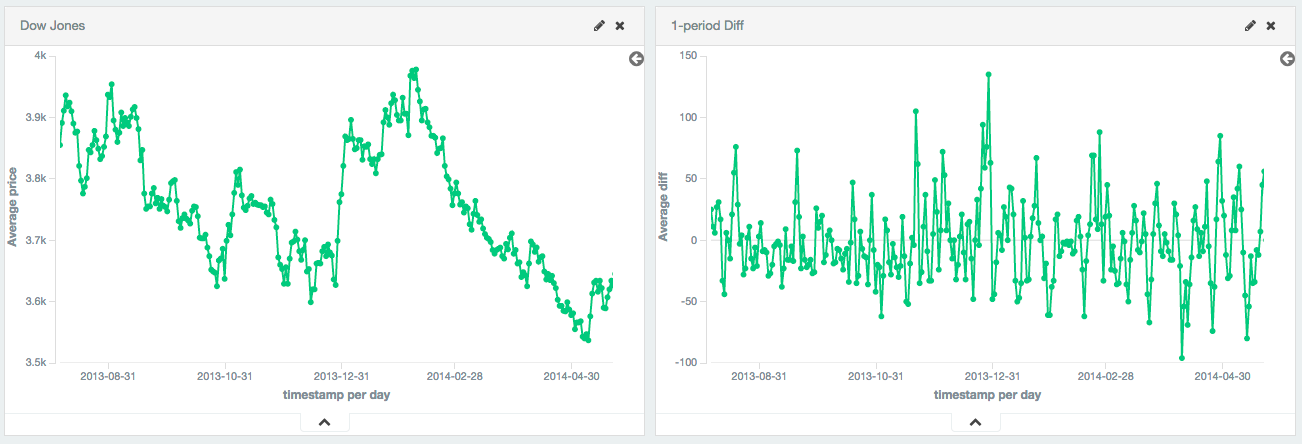

Single periods are also useful for transforming data into a stationary series. In this example, the Dow Jones is plotted over ~250 days. The raw data is not stationary, which would make it difficult to use with some techniques.

By calculating the first-difference, we de-trend the data (e.g. remove a constant, linear trend). We can see that the data becomes a stationary series (e.g. the first difference is randomly distributed around zero, and doesn’t seem to exhibit any pattern/behavior). The transformation reveals that the dataset is following a random-walk; the value is the previous value +/- a random amount. This insight allows selection of further tools for analysis.

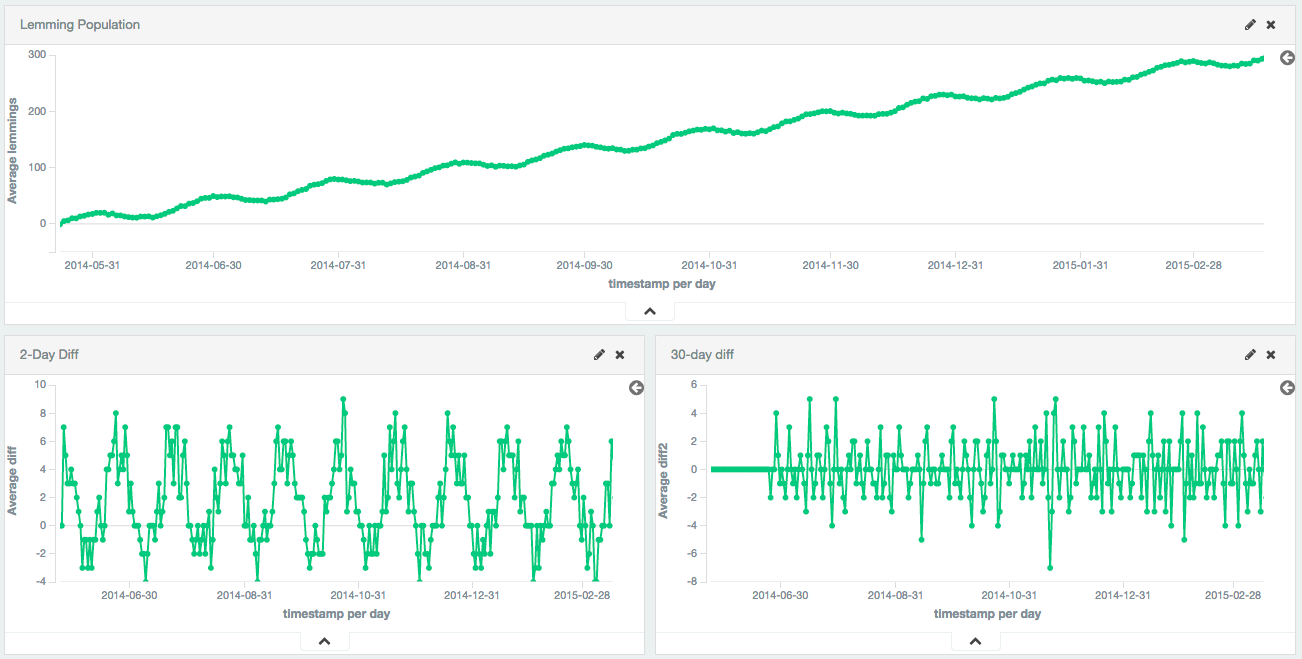

Larger periods can be used to remove seasonal / cyclic behavior. In this example, a population of lemmings was synthetically generated with a sine wave + constant linear trend + random noise. The sine wave has a period of 30 days.

The first-difference removes the constant trend, leaving just a sine wave. The 30th-difference is then applied to the first-difference to remove the cyclic behavior, leaving a stationary series which is amenable to other analysis.

Syntaxedit

A serial_diff aggregation looks like this in isolation:

{ "serial_diff": { "buckets_path": "the_sum", "lag": 7 } }

Table 77. serial_diff Parameters

| Parameter Name | Description | Required | Default Value |

|---|---|---|---|

|

Path to the metric of interest (see |

Required |

|

|

The historical bucket to subtract from the current value. E.g. a lag of 7 will subtract the current value from the value 7 buckets ago. Must be a positive, non-zero integer |

Optional |

|

|

Determines what should happen when a gap in the data is encountered. |

Optional |

|

|

DecimalFormat pattern for the

output value. If specified, the formatted value is returned in the aggregation’s

|

Optional |

|

serial_diff aggregations must be embedded inside of a histogram or date_histogram aggregation:

POST /_search { "size": 0, "aggs": { "my_date_histo": { "date_histogram": { "field": "timestamp", "calendar_interval": "day" }, "aggs": { "the_sum": { "sum": { "field": "lemmings" } }, "thirtieth_difference": { "serial_diff": { "buckets_path": "the_sum", "lag" : 30 } } } } } }

|

A |

|

|

A |

|

|

Finally, we specify a |

Serial differences are built by first specifying a histogram or date_histogram over a field. You can then optionally

add normal metrics, such as a sum, inside of that histogram. Finally, the serial_diff is embedded inside the histogram.

The buckets_path parameter is then used to "point" at one of the sibling metrics inside of the histogram (see

buckets_path Syntax for a description of the syntax for buckets_path.

On this page